Peter Ryan* reports on a draft report from the Productivity Commission that finds super fund members are being short-changed billions of dollars every year.

Australia’s superannuation system is “an unlucky lottery” for many members, with retirement nest eggs being diluted by unnecessary fees and underperforming funds, according to a landmark study out last week.

Australia’s superannuation system is “an unlucky lottery” for many members, with retirement nest eggs being diluted by unnecessary fees and underperforming funds, according to a landmark study out last week.

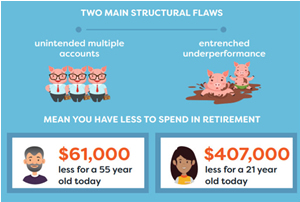

A highly critical draft report by the Productivity Commission into Australia’s $2.6 trillion superannuation system has delivered a mixed report card warning that multiple super accounts and sub-par funds that are “entrenched underperformers” are costing members $3.9 billion every year.

One in four funds have “persistently” fallen short of the mark over the past decade, the report says, meaning around 5 million member accounts are being short-changed with a new member potentially losing $375,000 by retirement.

The report by the Federal Government’s peak economic advisor says by eliminating multiple accounts and switching to a better-performing fund, a 55-year-old could gain $61,000 by retirement and that new entrant could build a $407,000 retirement account by 2064.

Productivity Commission Deputy Chair, Karen Chester said the architecture of the compulsory superannuation system introduced by former Labor Prime Minister Paul Keating in 1992 is “outdated” and suffers from structural flaws.

“We’re 27 years down the track from when compulsory super was introduced in Australia so it’s time to modernise and time to get rid of these two fundamental flaws that are causing members great harm,” Ms Chester told the ABC’s AM program.

“While the system works reasonably well for some members, it’s become an unlucky lottery that sets the odds against many members.”

“The impact is highly regressive.”

“It causes great harm to young people, workers on low incomes and workers in and out of the workforce.”

“These are awkward truths that the industry needs to address.”

The superannuation industry has been criticised for being on “a gravy train” since the early days of compulsory superannuation and has reaped billions of dollars in fees each year.

Ms Chester said that with a healthier population and retirees living longer, there was a risk that without reform some retirement funds could be drained, putting pressure on the aged pension entitlement.

“The main objective of the super system in accumulation is to make sure that members retire with the biggest balance possible,” Ms Chester said.

“But if those balances are being eroded by these two problems — unintended multiple products and underperforming products and funds — then they’re not going to retire with the biggest possible balances.”

A key recommendation is that workers should be allocated a single default product from a “best in show” list when they enter the workforce to avoid multiple funds.

The report says around one-third of accounts in the system are multiple accounts and erode members’ balances by $2.6 billion a year in unnecessary fees and insurance.

The report also recommends that employers lose their obligation to choose a default fund for their compulsory contributions given concerns that some employers might have a conflict of interest in managing worker nest eggs.

“It’s an inevitable conflict of interest,” Ms Chester said.

“Employers are meant to be looking after their business or their shareholders.”

“They don’t have a legal obligation to their employees.”

Super ‘worse than honey pot’, Minister says

Financial Services Minister, Kelly O’Dwyer said the draft report highlighted real problems with duplicate accounts and erosion of superannuation fund balances through fees.

“This report shows the super system has not been working as effectively as it should for millions of Australians,” Ms O’Dwyer said.

“The default arrangements are broken for those people who don’t choose where to put their money.”

“Super has become worse than a honey pot; it’s a trough.”

“The significance of superannuation to the wellbeing of all Australians cannot be overstated.”

Do industry funds still outperform retail funds?

The report also questions the claim that industry superannuation funds always outperform retail funds and says that some industry funds are also among the underperformers.

“Industry funds on average have clearly outperformed retail funds over the past decade but unfortunately for fund members they don’t all enjoy the average experience,” Ms Chester said.

Ms Chester agrees that given the complex and confusing nature of superannuation, the industry needs to do a better job in communicating the need for better options with members.

“Members are really lost in the weeds of product proliferation with 40,000 products,” Ms Chester said.

“They’re bamboozled by poor disclosure and we know from ASIC [Australian Securities and Investments Commission] poor advice.”

In addition to blasting the current system, the report touches on the controversial issue of insurance within superannuation, which many members don’t know they have.

“Not all members get value out of insurance in superannuation,” Ms Chester said.

“Many see their retirement balances eroded — often by $50,000 — by duplicate, unsuitable or even zombie policies.”

The Commission also calls for stronger governance rules for funds, a recommendation certain to be jumped on by Ms O’Dwyer, who has been pushing for an overhaul of trustees on industry funds to ensure one-third are independent.

The financial services Royal Commission is set to examine the superannuation industry later this year with a focus on complaints about both retail and industry funds.

* Peter Ryan is the ABC’s senior business correspondent. He tweets at @Peter_F_Ryan.

This article first appeared at www.abc.net.au.