Amelia Lester* says the Barefoot Investor’s universal appeal comes from his message that money is a means to an end, and that end is the ability to live the way you want.

After 26 years of uninterrupted economic growth — possibly the longest stretch of any developed country in modern history — you’d expect Australians to feel pretty relaxed about their pocketbooks.

After 26 years of uninterrupted economic growth — possibly the longest stretch of any developed country in modern history — you’d expect Australians to feel pretty relaxed about their pocketbooks.

Yet the biggest-selling nonfiction title on record in Australia concerns — of all things — personal finance.

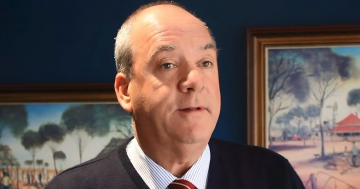

In a country of 24 million people, Scott Pape (pictured) has sold more than one million copies of The Barefoot Investor: The Only Money Guide You’ll Ever Need since its publication in December 2016.

Even more extraordinary than those sales figures is the devotion of Mr Pape’s followers.

They use terms like “splurge card” (a debit card for everyday luxuries), “mojo account” (for when you feel like quitting your job) and “fire extinguisher funds” (emergency reserves) with an enthusiasm not normally associated with fiscal responsibility.

Part of Mr Pape’s appeal probably comes from the fact that so many Australians are happy to have more money than they’d expected, but it’s also a function of just how Australian he is.

This is surely the only money guru who begins his book with the image of a charred sheep nearing death, one of the casualties of a devastating wildfire that destroyed his farm outside Melbourne in 2014.

But his message, that money is a means to an end, and that that end is the ability to live the way you want, has universal appeal.

“At some stage you’re going to face your own financial fire,” writes Mr Pape, who at the time of his disaster was a TV talking head on investment strategies.

“The goal of the Barefoot Investor can be summarised in one word: control.”

His tone is relentlessly casual.

At the end of each chapter, he encourages the reader to head to the pub.

“Money talk is better with garlic bread and wine,” he writes.

Throughout, he displays a suspicion for authority and a disdain for the wealthy, which syncs with the Australian national mythology of a classless society.

On the phone from his farm, Mr Pape is clear on what his book is not.

“It isn’t a wealth creation book which will make you a millionaire,” he said.

“It’s about security.”

He’s “barefoot” because that’s how life was for him growing up in a rural area, working alongside his father who ran and later owned a petrol station.

After a business degree at a regional university, Mr Pape worked for a short time as a stockbroker in Melbourne before starting his own financial advising business.

“I went into finance not for the wealth … but because I wanted to keep my freedom,” he said.

Ten years ago, he started writing a syndicated newspaper column on personal finance.

Mr Pape’s folksy manner delivers down-home truths: don’t get swept up in trendy investments; pay off your debts; analyse how banks are managing your money.

As a result, it’s uncontroversial with experts.

Chris Richardson, an economist at Deloitte in Canberra, said Mr Pape’s major tenets, like his argument that Australians have generally overvalued property and undervalued stock trading, “are more real then people realise.”

Another cornerstone of the Barefoot Investor’s plan that resonates with economists is the importance of renegotiating bank fees, which, according to the Reserve Bank of Australia, run to $480 per household per year.

Danielle Wood, an economist at the Grattan Institute sees high bank fees as a result of status quo bias, or the tendency to accept things the way they are.

“I think the message of the Barefoot Investor gets traction because he encourages people to think about things, and think about why they’re paying too much,” she said.

Jackie Frankel, a factory worker from the Mornington Peninsula, is a zealous Barefooter, as Mr Pape’s fans are known.

She concedes that her two grown daughters don’t completely understand his appeal.

“They say to me, it’s common sense stuff to figure out what you owe, but I say people need it in black and white,” Ms Frankel said.

After reading the book, she and her husband started going out for “date breakfasts.”

After talking it through over eggs, they moved their money from one of the “big four” banks to an online-only account recommended by name in Mr Pape’s book.

“We saved $500 a month just doing that, and now we’re going to New Zealand on a cruise,” Ms Frankel said.

Mr Pape advocates for letting the good times roll by divvying money into “buckets.”

This approach ensures daily expenses are separated from “splurges,” like lattes, and “smile” purchases, which, like vacations, make you smile when you think of them.

Call it the set and forget principle of money management.

“He doesn’t subscribe to the idea that you’ve got to get down to the bare bones and have no fun,” said Ali Cusack, a Melbourne lawyer.

“He just says, build it into your budget.”

Ms Cusack has been to Europe each summer for the past two years and recently started her own maritime law practice.

“I got so ridiculously good at saving money that I didn’t even need to take out a loan to start my own business,” she said.

Even hearing these stories, it can be hard to grasp why Mr Pape seems to inspire such joy.

He is, after all, talking about money.

But then he shared a Facebook post on the Barefoot Invester page from Tania Drummond, a single mother of four, who wrote that one morning five of the 10 fellow patients in an oncology hospital ward where she was were reading Mr Pape’s book.

They were laughing and sharing their stories of mojo accounts and how they had implemented other aspects of Mr Pape’s personal finance strategy; it was the first time in a while that she could remember laughing.

Ms Drummond said Mr Pape talks in terms she understands, and that “he makes you feel like you’re doing something right, not something wrong”.

“Financial advisers often say, well, if you don’t have $150,000, I don’t want to speak to you, but Scott doesn’t make you feel embarrassed about what you have.”

* Amelia Lester is an Australian writer living in Japan. She tweets at @ThatAmelia.

This article first appeared at www.nytimes.com.